Mar 2, 2016

Welcome to our first episode focused on Bitcoin, digital

currency, and the blockchain. My guest is one of the most

thoughtful people anywhere on this topic and on payments overall:

Circle CEO and Founder Jeremy Allaire.

I met with Jeremy at his office in south Boston's "Innovation

District," a few blocks from where I live myself. They have

quintessential startup space in an old brick warehouse, and we sat

down on a New England winter day for a really fascinating

conversation.

I often talk about the five huge technology trends that are

revolutionizing financial services. Number 4 on my list is digital

currency. Not long ago, even senior leaders in banks and regulatory

agencies dismissed Bitcoin as insignificant and weird at best, and

dangerous at worst. Today, many people still think it's weird and

dangerous, but no one thinks it's unimportant. I'm going to assume

our listeners know the basics - that Bitcoin invented the

"blockchain," which is an open "distributed ledger" of

transactions, visible on the internet, and that being on the

internet makes it (like everything else there) instant and free.

Most people also understand that this can transform our slow,

high-cost payments system, and also any other system that is, in

effect, a chain of transactions or records. Most people also know

the blockchain record is unfakeable, unbreakable, and again,

visible - attributes that can fundamentally change how we organize

things from money and contracts and legal titles to operational

systems and markets of all kinds.

I once wrote a blog post called

"The Benefits of Bitcoin", arguing that the cheap and instant

movement of money can bring incredible upside potential for

financial consumers, as well as new risks. It will eventually

change everything from remittance services to the struggles facing

people on tight budgets who now rely on cash, since it's the only

way to be sure a bill gets paid exactly when it's due.

As understanding of Bitcoin has spread, a new conventional

wisdom has emerged - the notion that the crucial innovation here is

not digital currency, but rather the blockchain, including closed

chains inside companies and closed networks. In our conversation,

Jeremy challenges that idea head-on. He argues passionately that

the big power in this technology is its openness.

He reminds us, for one thing, that the internet initially

spurred hot debate over how to secure the unprecedented free-flow

of information. In a

widely-circulated article on re/code.com last

November Jeremy wrote, "Remember, the Internet was

unreliable, insecure, and filled with creeps and hackers. People

wanted safe, secure, trusted and proprietary networks. That was the

future...(yet) We all know what happened. Smart creators and

engineers from all around the world got inspired by the open

Internet...Permissionless innovation took hold, and we changed the

world." He thinks we now need to take the basic DNA of the Internet

- open protocols and distributed and decentralized networks - and

apply them not just to sharing data and information, but to the

sharing of value.

He also emphasizes a core power of this - the fact that if

you don't have to trust a single centralized institution to

facilitate value exchange, amazing things become possible. Jeremy

refers to bitcoin as a distributor of trust, one that "provides a

highly secure ledger to exchange value around the world." He

believes that just as the early Internet disrupted media and

communications, this wave of innovation will transform the "trust

and assurance" industries - "which includes government, law,

accounting, insurance and, last but not least, finance."

Entering into a global economy in which everything from

social identities to commerce flow instantly and freely is

discomfiting to some. Even though today's closed and proprietary

technology and networks create frustration and high costs for

consumers, Bitcoin critics still doubt the soundness and resilience

of the model. For innovators like Jeremy, though, it is creating a

whole new set of solutions that use financial technology to build

"smart rules" and business logic that can eventually shape the new

laws of global commercial and legal governance.

Jeremy's "aha" moment on this came in 2012, and inspired him

to start a company that would use blockchain technology, which he

calls the "global trust and transaction ledger," to change the way

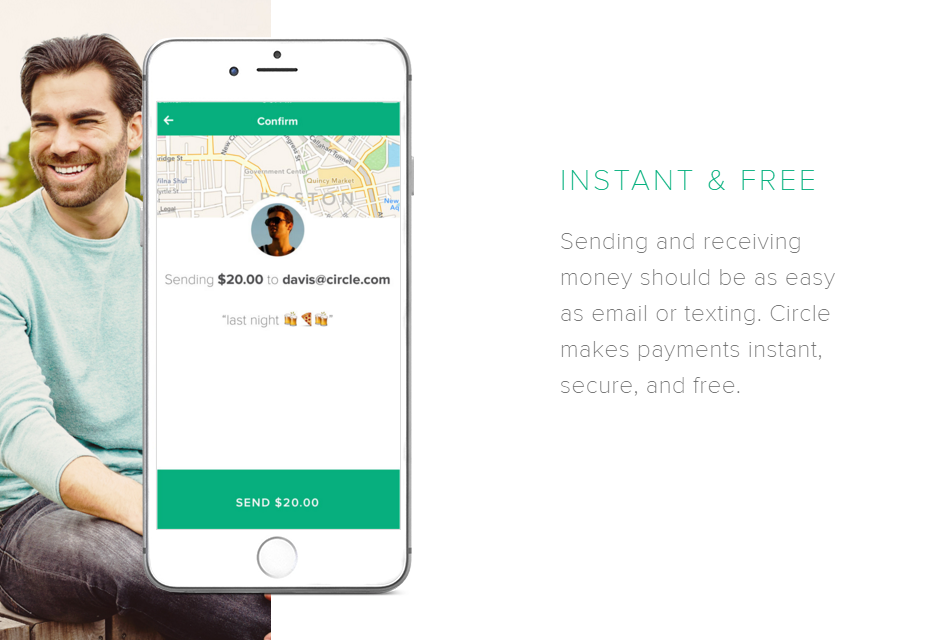

we store and use money. That company is Circle, a provider of

mobile apps "aimed at enabling greater ease-of-use in online and

in-person payments, enhanced security and privacy for customers,

and the convenience of free, instant, global digital money

transfers." A revolutionary idea. As I say in our conversation, I'm

a Circle customer myself. Every time I use it, it amazes

me.

Before Circle, Jeremy was an entrepreneur who'd already spent

two decades building and leading global technology companies. His

first startup, Allaire Corp, pioneered the use of the Web as a

platform for commerce and business applications, and grew to serve

over 1 million customers around the world. In 2000, Allaire Corp

was acquired by Macromedia, where Jeremy became Chief Technology

Officer and helped transform Flash into a platform for rich

applications and video that became the most widely adopted piece of

software in the history of computing.

He then founded Brightcove, the first Internet video

publishing platform for websites, smartphones, tablets and

connected-TVs. The company has customers in more than 100 countries

and powers video operations for 25 percent of the top 10,000

websites in the world. From 2003 to 2014, Jeremy also served as a

Director at Ping Identity Corporation, an industry-leading software

and online service provider for securing identity on the Internet

whose clients include many of the largest financial institutions in

the world.

In our conversation, Jeremy explains his vision, his long

background in technology, how Circle works, their business model

and plans, and his thoughts about regulation of finance and

fintech. The regulatory challenges are obviously huge. Circle

sought and received the first-ever (and at this writing, still

only) New York State "bit-license." Jeremy talks about the

challenges of becoming licensed as a money transmitter in the U. S.

state-by-state regulatory patchwork. He also recognizes that,

importantly, governments throughout the country and the world see

potential as well as risk in these innovations. An example is that

Jennifer Shasky Calvery, Director of the Financial Crimes

Enforcement Network, has

testified before Congress that

FinCENrecognizes the "potential for abuse by illicit actors," and

that the agency has for almost five years worked with its

regulatory partners on designing rules that provide the "needed

flexibility to accommodate innovation in the payment systems space

under our preexisting regulatory framework."

Jeremy Allaire has an exceptional gift for making

mind-bending technology and regulatory challenges easy to

understand - and for provoking thought. This is, without a doubt,

one of the most fascinating episodes we've had.

Enjoy it, and please be sure to click the "Donate" button

HERE, and to write a review on ITunes, to keep supporting the

show.

And.....Introducing my video series: Regulation

Innovation

Meanwhile, I have a video for you -- two of them,

actually.

Many listeners know I have long been a consultant to the

financial industry, first on regulatory matters and more recently

on fintech. A couple of years ago, someone suggested that I take

the kind of advice people pay me for as a consultant, and distill

it into video briefings that are accessible and affordable for a

much wider market. It was a great idea, and so I began building a

video series offering my advice.

I've focused the videos on the most important question facing

consumer financial services -- How to survive, and actually thrive,

through the twin disruptions that are hitting the industry:

technology innovation, and regulation.

I think everyone in fintech will enjoy them, but the series

is specifically designed as a guide for financial companies - it's

informative, thought-provoking, and practical. It's for both

traditional companies and innovators. And it's for the people

working on innovation, regulation, and building the

business.

I am very confident in saying there is nothing else remotely

like it. Please check it out!

And while you're there, check out my little bonus video

because it answers, at long last, this burning question: "Why does

Jo Ann Barefoot have an Xbox, since she's never played a videogame

in her entire life, and what the heck does this have to do with

financial innovation?"

www.regulationinnovation.com.

See you there!

If you enjoy our work to bring together thought provoking ideas and people please consider a contribution to support the site.

Support the PodcastPlease subscribe to the podcast by opening your favorite podcast app and searching for "Jo Ann Barefoot", in TuneIn, or in iTunes.